17 The Record Industry Today

The record industry today is dominated by three large, multinational media conglomerates (Universal, Sony, and Warner) that collectively earn over 70% of the revenue of the entire industry. Independent record companies make up most of the other 30% of revenue and, as always, they play an important role in releasing new artists and genres that the major companies often ignore (folk, classical, bluegrass, jazz, etc.). Note that each of these major record companies also earns a significant amount of their revenue from non-music sources, such as movie production. For example, Sony’s 2017 music-related total sales of $800 million comprise less than 10% of its company-wide revenues. This highly diversified portfolio of revenues demonstrates the attraction of consolidation to an industry that has faced multiple financial downturns. Sony and the other major media companies can survive the disruptions and ups and downs inherent in the music industry without worrying that the ship will sink, as some other unit in the company will likely provide ballast.

Another segment of the the record industry, which only makes up about 3% of total revenue, is nonetheless worth mentioning: self-released records and the internet-based companies that support them. Founded in 1998, CD Baby was the pioneer in this market segment, originally providing CD manufacturing, marketing and distribution services to musicians who did not have the support of a record company. With the advent of internet streaming, CD Baby has made the transition to offering that same level of support to musicians to get their music on the internet and onto streaming services. For a fee, CD Baby and other companies that have followed in its footsteps, such as DistroKid and SoundCloud, can offer musicians many of the services provided by a record company other than the up-front cash advance. The services provided by these companies rarely result in significant earnings for musicians, but they offer a potential point of transition to artists who can quickly build a following and then attract the attention of a traditional record company.

There are two glaring holes in this description of today’s music industry that I will now address — YouTube and live music. I will only briefly touch on these topics in this chapter because I will discuss in them in greater detail later in the book. First, YouTube. YouTube is its own legal and financial universe and does not fit neatly into any other segment of the industry. But YouTube has nearly two billion users per month (!), and, according to Google (YouTube’s owner), it paid out $3 billion in total revenue to the music industry in the year ending September, 2019.

YouTube functions more like the P2P file-sharing companies than it does any other music distribution model, with the major difference being that its revenue is derived almost entirely from advertising. YouTube is also legally protected from copyright infringement complaints due a law, the Digital Millennium Copyright Act, that we will discuss in a later chapter. Like P2P services, YouTube does not provide content to is users, other users do. YouTube hosts the shared files on its own servers, but it does not create them or pay to have them on the service. It only shares ad revenue with those who post the videos based roughly on the number of streams. Because of this difference, YouTube does not pay licensing fees or other legally-mandated fees to record companies or musicians for the music used on YouTube videos. Accordingly, YouTube pays much less per stream to music creators and rights holders than do music streaming services such as Spotify. And YouTube is not a profit center for Google as it apparently loses over $100 million per year according to Google. (YouTube and Google are subsidiaries of parent company Alphabet, which is not required to report the earnings data for those subsidiaries, only for the parent company as a whole. However, Alphabet voluntarily began providing more financial data on YouTube beginning in 2019.)

Another striking change in music industry revenues is the rise of live music ticket sales, which now make up the vast majority of most performing musician’s incomes rather than sales of recorded music. Each spring, Billboard magazine publishes a list of the top-50 highest grossing musical acts of the previous year, breaking down the sources of their income. A quick look at the most recent such list shows how critical live performance revenue has become in comparison to recorded music sales: Taylor Swift was the top grossing musical performer in 2018, earning $99.6 million in the year. Of this, $90 million, or over 90%, was earned through live performances. Only about 5% of this came from streaming of her music! The second highest grossing act was Bruce Springsteen with a total of $53 million in revenue, of which over 95% came from touring and less than 3% from streaming and sales. Drake was 2019’s leader in streaming revenue, but even for him that figure made up only less than a third of his total revenue. For all other performers on the list, the disparity between live performance revenue and sales revenue is even more striking.

The Recording Industry Association of America (RIAA) provides annual financial data about the health of the recording industry (and mid-year updates). Using the latest full data set from 2018, supplemented by a 2018 report on the industry issued by CitiBank, here as a summary snap shot of the industry:

- Revenues. In terms of gross revenue, the music industry has recovered from both MP3 piracy and the 2008 “Great Recession”. Total music industry revenues in 2017 were equal to the previous music industry revenue peak of 2006. However, the source of those revenues has changed dramatically: In 2006, the vast majority of music industry revenues came from sales of CDs. Today, the vast majority of revenue comes from streaming (75%), followed by live concert ticket sales. Sales of physical product are a distant third place as a revenue category. In the streaming category, paid subscriptions make up 75% of streaming revenue as compared to ad-based revenue.

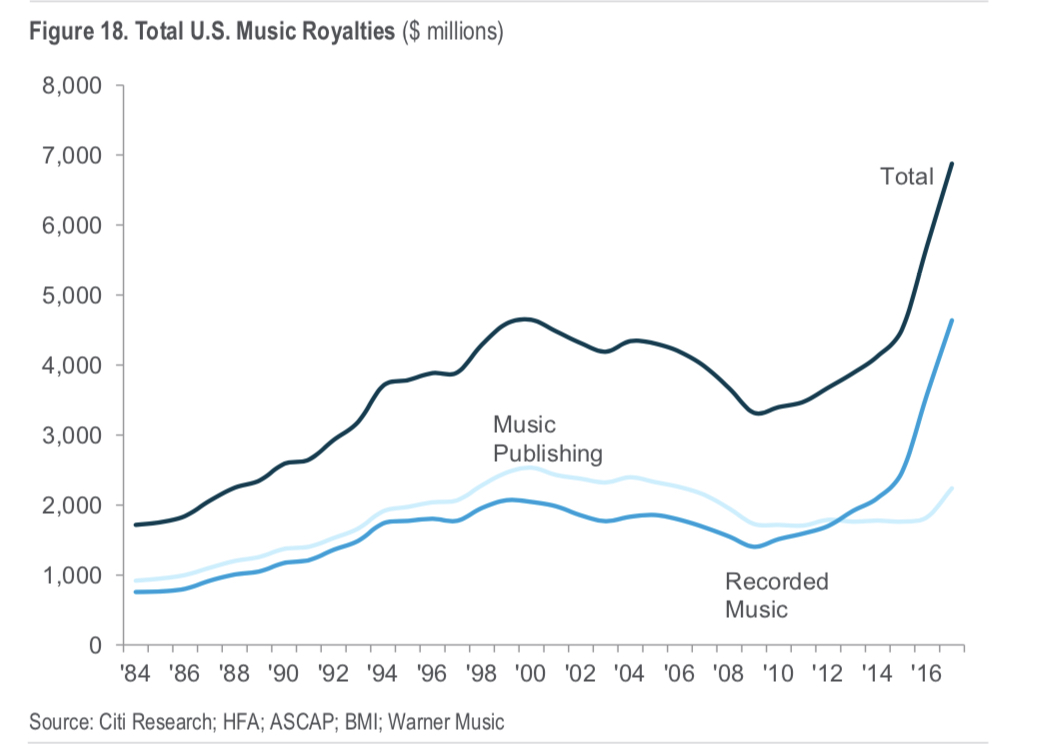

- Royalties. Another change reflected in the recent data is that, beginning in about 2013, royalty income paid to the holders of sound recording copyrights has exceed the royalties paid to the holders of song copyrights. Prior to this change, songwriters had always been more highly compensated from royalties than recording artists and their record companies. However, due to differences in the way royalties are calculated from streaming versus sales of music, songwriters now earn significantly less. This change may be reversed in the years to come due to changes in song copyright royalty calculations from streaming contained in the Music Modernization Act of 2019. We will explore the details of this change in the chapter on music royalties.

- Streaming versus Downloads. As streaming revenue has risen in recent years, revenue from digital downloads of music has decreased sharply. As consumers have become streaming service subscribers, there is no longer a demand to own, rather than rent, songs. Most music consumers now pay an “all you can listen to” monthly music rental fee. Accordingly, Apple has discontinue its iTunes app (now replaced by the Apple Music streaming app), and no longer sells song downloads.

- Physical Sales. Sales of all physical recorded product (CDs and vinyl records) declined over 35% from 2017 to 2018. Bucking this trend, sales of vinyl records increased over 12% in this period, but the total volume is far too low still to make up for the decline in CD sales.

- Revenue to Artists. In 2018, 42% (approximately $18 billion) of industry revenue went to artists and their record companies. However, of this, only about $5 billion, or 12% of total industry revenues, went directly to artists. Despite this seemingly small number, this represents an historic high mark for both the share of revenues and absolute dollar amount being distributed to artists. Another sobering statistic is that, despite the increasing revenue associated with streaming, artists make very little from this source. As Spotify’s revenues have increased, the amount paid to artists per stream has decreased. At the current rate (as of 2018), it would take 312,827 streams for an artist to earn $100 from Spotify!

- Costs of Internet Distribution and Delivery. The largest category of costs in the music industry currently is the approximately $15 billion associated with running music delivery platforms on the internet (Pandora, Spotify, Apple Music, etc.). This fact helps explain why streaming sites such as Spotify continue to be unprofitable despite their large and rapidly increasing base of users.